In partnership with

|

S&P 500 FUT

7,456.00

▲ +0.21%

|

NASDAQ 100 FUT

24,225.00

▲ +0.24%

|

GOLD

$4,039.50

▲ +0.02%

|

|

BRENT CRUDE

$73.22

▲ +0.10%

|

VIX

17.49

▼ −0.91%

|

BITCOIN

$59,150

▼ −0.55%

|

|

Lauren Collins

Human-augmented AI editor covering macro · Atlas360° Morning Briefing

|

| DIPLOMACY U.S.-Iran talks, Doha. Envoys Kushner and Witkoff are in Qatar, yet Washington and Tehran can't agree on whether a formal meeting even happens today. A confirmed sit-down calms oil; a walkout snaps the war premium back. |

| DATA · 10:00 ET U.S. consumer confidence (June). Consensus around 92.0 after May's 93.1. A soft tape-off would test the "resilient consumer" story just as the Fed leans hawkish on prices. |

| DATA · 9:45 ET Chicago PMI (June). Consensus near 51 after May whipsawed to 62.7 from 49.2. A reversion below 50 would say the May jump was noise, not a manufacturing turn. |

| EARNINGS · AFTER CLOSE Nike (NKE), fiscal Q4. Consensus near $0.12 EPS on about $10.85bn in revenue, down roughly 2% y/y. The read on China demand and the turnaround plan will matter more than the print. |

| FLOWS Quarter- and half-end rebalancing. Pension and index resets land into thin liquidity, with Thursday's jobs print and a closed Friday ahead. Expect outsized moves on light volume. |

Central Banks Bury the Rate-Cut Era as Sintra Turns Hawkish

01 |

U.S. and Iran Send Mixed Signals on Doha as the Truce HoldsThe weekend standdown is holding; the diplomacy is a fog. Trump says Tehran requested a Doha meeting today and is sending Kushner and Witkoff; Iran's foreign ministry says nothing is scheduled, its team there only to verify the memorandum before real talks resume. Brent took the calmer read, easing to about $73. Still untouched: Iran's enriched-uranium stockpile and sanctions-relief terms. Watch whether a Doha meeting convenes: confirmation steadies oil, while a snub or a Hormuz incident is the fast track back to a $90 print.

|

02 |

China Factories Grow Again, Carried by the AI Build-OutJune's official manufacturing PMI hit 50.3, beating forecasts for a third straight month above the line, with new orders back to expansion (51.2) and the high-tech gauge at 53.5. But factory-gate prices fell for the first time in six months and hiring stayed soft. Watch whether output-price deflation pulls Beijing toward stimulus; until it does, the rebound is narrow and the yuan on a short leash.

|

03 |

The AI Trade Meets a Fed That Won't CutEurope's chip names ran hard at the open, ASML up 3.2%, on the AI demand that lifted China's high-tech PMI. Nvidia's RTX Spark push into Windows PCs has helped Microsoft, Dell and HP while knocking Intel, AMD and Qualcomm: the rally is share-stealing now, not a rising tide. The catch is the discount rate: every multiple here was built on cheap money, and a Fed flagging hikes raises the cost. Watch mega-cap tech into Thursday's jobs print: if yields jump, the leaders of the half lead the unwind.

|

Where to Invest $100,000 Right Now, According to Experts

Investors face a dilemma. When the S&P 500 finished its worst quarter since 2022 last month, diversifiers like bonds and bitcoin fell too.

Even with the turnaround in mid-April, analysts at Goldman Sachs and Vanguard have projected low-single-digit annualized returns from 2024-2034.

Bloomberg asked where experts would personally invest $100,000 for their March monthly edition.

One answer that surfaced for a second time? Art.

It's what billionaires like Bezos and the Rockefellers have privately used to diversify for decades.

Why?

Appreciation. The ArtPrice100 Index outpaced the S&P 500 overall from 2000 to 2025

Low-correlation. The postwar contemporary segment has moved independently of traditional investments like stocks since ‘95.*

Resilience. A scarce, physical, and global asset class with decades of demonstrated demand.

Thanks to the world's premier art investing platform, now anyone can invest in works featuring legends like Banksy, Basquiat, and Picasso, without needing millions.

Shares in new offerings can sell quickly but...

*According to Masterworks data. Investing involves risk. Past performance is not indicative of future returns. See important Reg A disclosures at masterworks.com/cd.

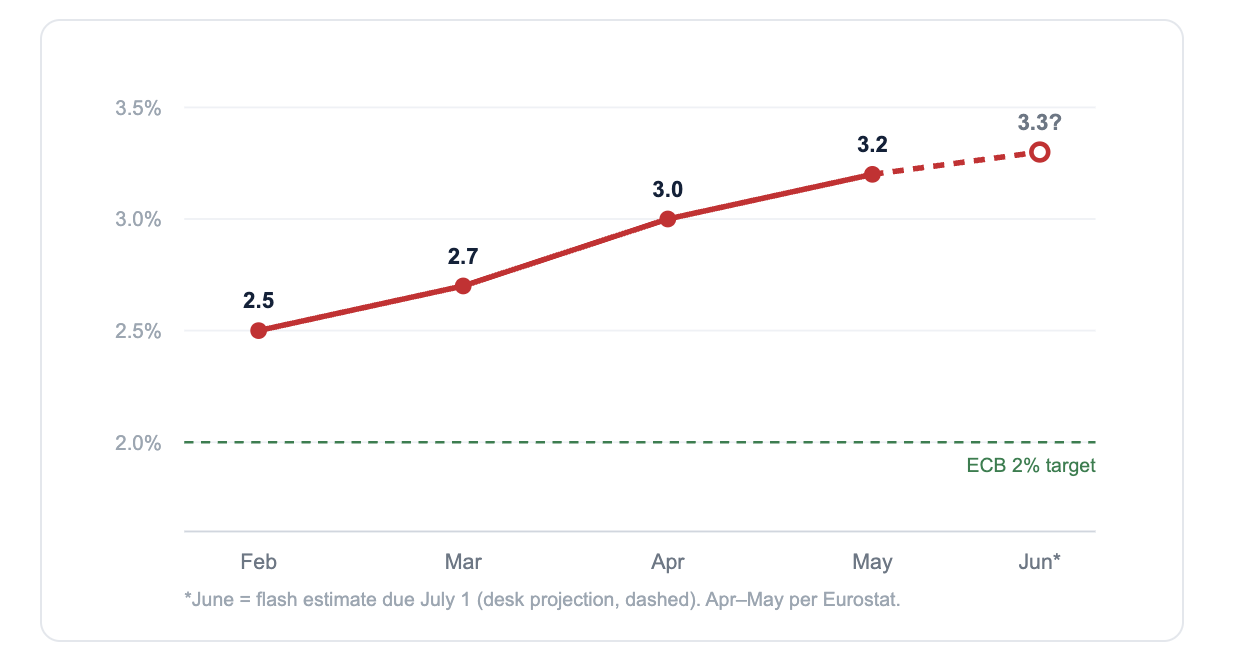

Europe's Inflation Is Climbing the Wrong Way Into Tomorrow's Flash

| Why it matters Headline HICP rose to 3.2% in May from 3.0% in April, energy up double digits and core stuck near 2.6%. That's the data behind Lagarde's hawkish turn. |

| Watch Tomorrow's June flash. Another tick up hardens the case for a July ECB move and squeezes the euro area's indebted south. |

| Source Eurostat flash estimates; June figure is a desk projection pending the July 1 release. |

| WASHINGTON A SpaceX stake for "Trump Accounts"? The White House is weighing seeding the new Trump Accounts with SpaceX stock, an unusual blend of federal policy and a private mega-cap that raises questions on valuation, conflicts and precedent. Watch how a non-public company would even be priced into a government program. |

| CRYPTO Bitcoin sat out the party. Near $59,100 and slipping while equities ripped, the token has decoupled from risk, exactly what you'd expect when the discount rate stops falling. A hawkish jobs print is the next pressure test. |

| CLIMATE & ENERGY A heat dome over 220 million Americans. An intensifying heatwave is pushing extremes across much of the country, straining power grids into peak cooling demand and firming near-term gas and power prices. Watch grid-operator emergency alerts and any drag on outdoor-dependent output. |

| HOUSING NYC moves on a pied-à-terre tax. Mayor Mamdani is advancing a levy on second homes, taking aim at absentee-owned luxury units, a revenue play with national resonance for housing politics and high-end real-estate values. Watch the threshold and whether it dents Manhattan's top-tier condo bids. |

| CULTURE & CAPITAL A Swift wedding could move Midtown. Rumors of a Taylor Swift wedding tied to a Madison Square Garden permit are enough to stir the events economy: hotels, security, ticketing and the Midtown small-business take that trails her everywhere. Watch whether the permit chatter is real; her footprint is a measurable demand shock. |

Atlas360° Media

Unsubscribe · Update preferences · View online